Patient Accounting Systems Disrupt Revenue Cycle Management

Hospitals must prepare for possible revenue cycle management and cash flow risk following PAS conversion. Careful planning and an assessment of resources are key for success.

- Most hospitals experienced a noteworthy revenue cycle management performance disruption following recent conversion of their patient accounting systems (PAS), according to a new Crowe Horwath benchmark report.

Technological innovations are powering greater efficiency levels and manifesting more value, the report said. The short-term effects of a PAS conversion – i.e. Epic or Cerner – may heavily impact cash flow.

Hospital leaders preparing for a conversion should anticipate billing and coding function disruption once the switch has gone live. But hospital leaders with adequate knowledge and honest expectation of what may happen to their cash collections and revenue cycle performance post-conversion may see better results.

“Although the long-term benefits of system conversion might outweigh short-term challenges of implementation, the additional costs associated with implementations that are not tightly managed can be substantial,” Crowe Horwath said.

These costs must be taken into account when determining how much the new software will cost, the organization said. It is possible “the hit to cash may be permanent,” researchers claimed.

“Hospitals should be prepared to absorb a temporary reduction of cash on their balance sheet equal to at least one month’s cash collection,” they said.

“Whether implemented as stand-alone packages or as components of a larger electronic medical record patient management system, [PAS] are some of the most sought-after solutions,” researchers wrote.

Patient account transactional data collected from over 500 hospitals into last December evaluated how cash collections and related key performance indicators (KPIs) were affected among 32 acute care hospitals that completed PAS conversion within the last three years.

“The effects of a PAS conversion can have a dramatic impact on a hospital’s revenue cycle,” stated Brian Sanderson, Managing Principal of Crowe Healthcare Services.

“Although the long-term benefits of system conversion might outweigh the short-term challenges of implementation, the additional costs associated with implementations can be substantial if they’re not tightly managed,” he said.

“To lessen the financial and operational risks of a PAS conversion, hospitals should not consider this to be only a technology implementation – but rather an operational and financial implementation that includes stakeholders from key clinical departments as well as finance leadership,” Sanderson added.

Key research focuses on three PAS stages

One of the report’s top findings was the number of accounts receivable days reportedly increased from 52 days to over 62. Secondly, the most interruption to billing and coding metrics apparently occurred within the first month. Third, discharged-not-final-billed (DNFB) days shot up by 86 percent. Lastly, it was determined the number of late charges increased six-fold.

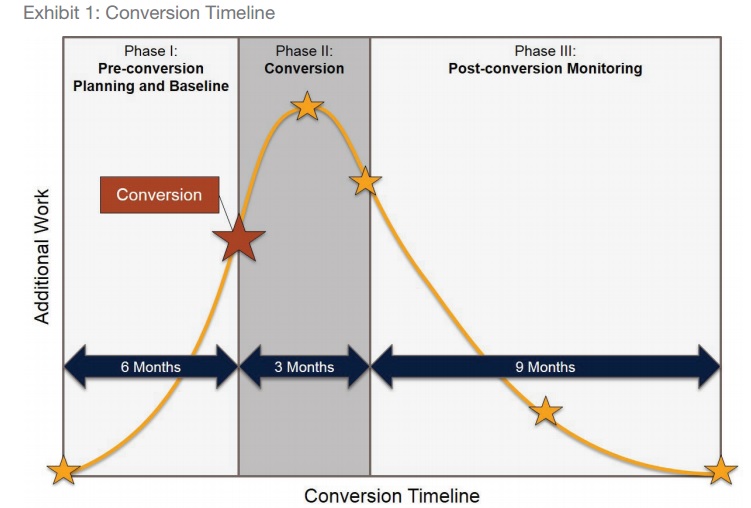

Hospitals were assessed across three general conversion PAS phases:

- Pre-conversion baseline: six months prior to PAS conversion

- Conversion: the three months post conversion period

- Post-conversion monitoring: an additional nine-month period

During the first phase, “planning work for the conversion is completed and baseline values for KPIs that will be used to monitor post-conversion performance are calculated,” the report explained.

Additionally, Crowe Horwath recommended implementing a variety of “quality gates” at this time.

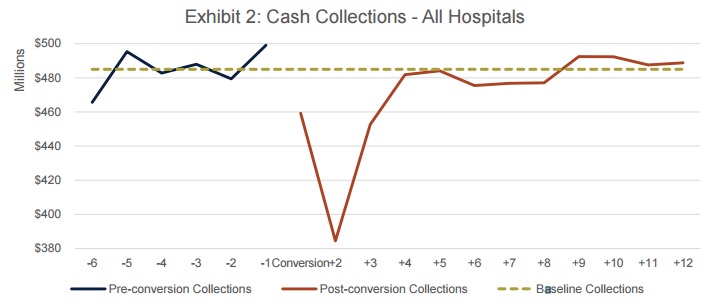

In Phase 1, hospitals’ monthly cash collections averaged $485 million. These hospitals had an average of 227 beds per hospital.

Within the month after conversion, cash collections reached a 12-month low and fell to over 20 percent below baseline collections.

Crowe Horwath said Phase II is essentially an “all hands on deck” approach as “the highest-intensity phase.”

In this phase, “the hospital will convert day-to-day patient accounting operations to the new program, implement plans for legacy AR … and go through a cleanup process of legacy credit accounts (accounts with negative balances) to help ensure income recovery opportunities are maximized and unclaimed property regulations are being followed appropriately,” said Crowe Horwath.

Throughout the remainder of the second phase, cash collections reportedly “dropped sharply” and fell below the baseline.

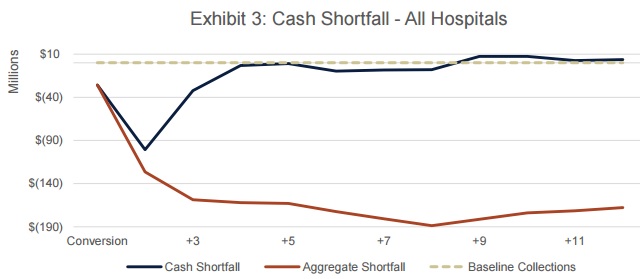

By the end of the second phase, the hospitals experienced a total cash shortfall of nearly $162 million.

The third phase is apparently when the revenue cycle is measured in comparison with pre-conversion baselines.

During phase three, monthly cash shortfalls hovered at below 10 percent below baseline.

There was reportedly a great deal of variation in hospital performance during this time.

“For many hospitals, the aggregate cash shortfall continued to increase steadily while several hospitals with stronger performances collected cash above the baseline level during Phase III,” said the report.

It was apparently not until post-conversation monitoring period nine months following the conversion that cash collections went back to where they started.

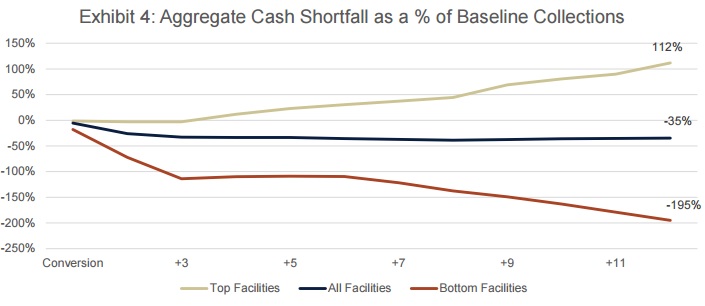

“Top performers, often those with a well-planned implementation strategy, experienced cash surpluses equal to 112 percent of baseline collections by the end of Phase III,” the report explained.

“Bottom performers experienced an aggregate cash shortfall nearly three times greater than the average at 195 percent below baseline collections, the equivalent of almost two months of collections.”

“Hospitals should be prepared to absorb a temporary reduction of cash on their balance sheet equal to at least one month’s cash collection. In some cases, the hit to cash may be permanent,” Crowe Horwath stated.

Hospitals should develop and execute a project management office and a detailed outline of what each phase of the conversion may look like, the organization advised.

Those hospitals without adequate resources should look outside of their four walls for assistance and consider outsourcing as a viable opportunity, they added.

“Patient accounting teams must have the necessary skills and capabilities to manage every aspect of the conversion and maintain the normal day-to-day functions of their patient accounting office,” they said.

“By enlisting the support of seasoned change management professionals with deep net revenue experience, hospitals can significantly reduce the risk to cash collections and revenue cycle performance post-conversion.”

Image Credit: [Crowe Horwath] (Conversion Timeline)

Image Credit: [Crowe Horwath] (Cash Collections)

Image Credit: [Crowe Horwath] (Cash Shortfall)