After a Slow 2017, ACOs Grow and Expand Their Contracts in 2018

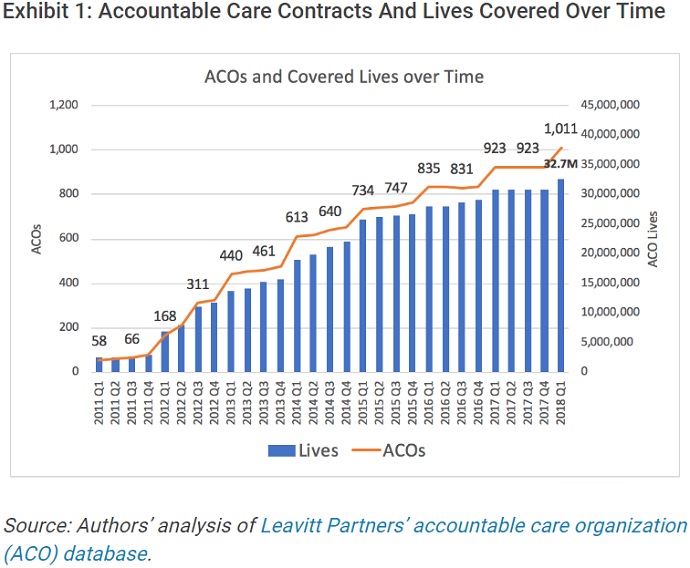

The number of accountable care organizations increased from 923 organizations in 2017 to 1,011 organizations by the start of 2018.

Source: Thinkstock

- The number of accountable care organizations (ACOs) continued to grow in 2018, as did the number of contracts the organizations entered, a new report from Leavitt Partners and the Accountable Care Learning Collaborative uncovered.

From 2017 to the end of the first quarter of 2018, Leavitt Partners and the Accountable Care Learning Collaborative tracked a total of 1,011 ACOs, the groups reported in a Health Affairs blog post.

The number of ACOs operating significantly increased from 923 ACOs in 2017. The data showed that ACO growth stagnated throughout 2017, with the number of ACOs remaining at 923 organizations until the start of 2018’s first quarter.

Source: Health Affairs

With over 1,000 ACOs running, the contracts covered about 32.7 million patients across the country by the start of 2018. The number of covered lives translated to about 10 percent of the US population, which increased six percent, or two million people, compared to the previous year’s estimates.

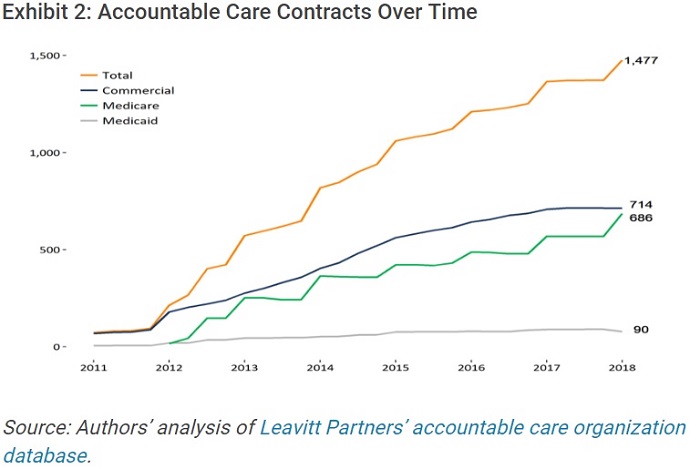

As more ACOs emerged, the number of contracts also increased, researchers pointed out. ACOs engaged in 1,477 distinct accountable care payment contracts with public and private payers by the end of the first quarter of 2018.

READ MORE: For Ongoing ACO Shared Savings, Look Outside Inpatient, Primary Care

ACO contracts with private payers led the pack, accounting for slightly over one-half of all ACO covered lives. Medicare and Medicaid followed, with Medicare ACO contracts representing 37 percent of covered lives and Medicaid ACO contracts accounting for 10 percent.

Researchers noted that commercial ACO contracts may cover more lives than Medicare ACO arrangements (24,300 versus 17,500 lives on average). However, the number of ACO contracts with private payers is almost equal to that of Medicare.

Source: Health Affairs

ACO contracts with private payers accounted for 48 percent of all the accountable care payment contracts in use by the start of 2018 and Medicare arrangements represented 46 percent of all contracts.

Medicare ACO contracts may have increased by the start of 2018, but the arrangements barely saw net growth during 2017. Medicaid also reported a modest contraction as state demonstration programs expired, researchers observed.

“Changes in federal administration and questions about whether and how the government would support VBP [value-based payment] models created significant uncertainty about ACOs,” they explained.

READ MORE: ACOs and Other Value-Based Purchasing Models Have Yet to Cut Costs

“Some providers we spoke with stated that they decided to take a ‘wait and see’ attitude toward developing new commercial contracts,” they continued. “Many health plans said that they were gradually and thoughtfully expanding their population health accountability programs given the federal uncertainty.”

While ACO growth in 2017 remained modest, organizations also dropped out of their contracts. From 2017 to the end of 2018’s first quarter, 232 ACOs formed. At the same time, 35 ACOs exited their respective arrangements with public and private payers.

Source: Health Affairs

Over 30 organizations may have quit their contracts because ACOs have struggled to improve performance while reducing their spending compared to their benchmarks, researchers explained.

For example, a 2017 Leavitt Partners and Duke-Margolis Center for Health Policy analysis found that quality performance in Medicare’s largest ACO model, the Medicare Shared Savings Program (MSSP), remained high with an average composite score of 93.4 percent in 2016.

However, only 56 percent of the 432 MSSP ACOs saved relative to their spending benchmark, and just 31 percent of the organizations saved enough to qualify for shared savings payments.

READ MORE: Key Issues Impacting Two-Sided Risk Accountable Care Organizations

“Many ACOs have not yet succeeded in improving performance while lowering spending trends relative to their benchmark, and more provider organizations may exit ACO programs in the future,” the recent Health Affairs blog post stated. “Learning more about the characteristics of those ACOs that leave will help inform program design.”

Recent changes to the MSSP may also prompt more ACOs to leave the program. Just before Leavitt Partners and the Accountable Care Learning Collaborative released their findings, CMS proposed to overhaul the Medicare ACO program by changing its name to Pathways to Success and reducing the amount of time organizations can stay in a shared savings-only track.

Critics of the proposal fear the accelerated risk timeline for participating ACOs will spur risk-averse organizations to exit the program because the Pathways to Success initiative does not give ACOs enough time to prepare for downside financial risk.

About 71 percent of MSSP ACOs nearing their time to take on downside financial risk and shared loss payments under the current iteration of the Medicare ACO program recently said they would quit the program rather than switch from a shared savings-only track.

In the most recent Health Affairs blog post, researchers explained that ACOs may be veering from the pathway because of the varying ways in which providers can succeed in alternative payment models.

“Hundreds of ACOs and other organizations are implementing a wide range of steps to try to succeed, and organizations show more success over time. But the mixed results and significant variation across organizations show that much work remains to identify what changes, interventions, and programs are most likely to achieve short-term improvements,” they wrote.

“In the meantime, many organizations may continue to struggle or remain uncertain about how to proceed, and some will continue to fall back to fee-for-service.”

The lack of business case and profitability assurance also hinders ACOs and other providers from continuing with alternative payment and care delivery models.

“Most provider organizations that have formed ACOs still have only a minority of their patients covered by alternative payment models and risk-based payments. Currently, ACOs see the need to experiment with risk-based payment models because they want to prepare for a potential future when such models are more prevalent,” the blog post stated.

However, ACO leaders are hesitant to transform their organization and workflows to align with downside risk models because the changes are not sustainable under fee-for-service, which is still the dominant payment model in the industry.

Only 29 percent of healthcare payments were reimbursed under an alternative payment model between 2015 and 2016, up just six percentage points from the previous year, revealed the most recent data from the Health Care Payment Learning and Action Network.

“To encourage organizations to change how they deliver care, the depth of risk is important, but perhaps more important is the breadth of risk — what share of revenue is under value-based payment arrangements,” researchers suggested.

“Accompanying a more compelling business case, organizations would benefit from clearer evidence and support for specific actions to succeed in the short term (the next one to three years),” they added. “Progress can be accelerated through collaborative learning and the development of more sophisticated and effective private- and public-sector supports to reduce uncertainty for providers.”

Value-based reimbursement and ACO programs are here to stay, researchers stressed. Despite stagnation in 2017, ACOs are growing and expanding as 2018 continues.

“Looking ahead, faster progress in care reform is possible. Public and private payers could refine payment models to provide a clearer path to success in taking on some financial risk and create a more coherent set of complementary payment reforms,” the blog post concluded. “Providers can seek to learn more from the organizations that are succeeding.”